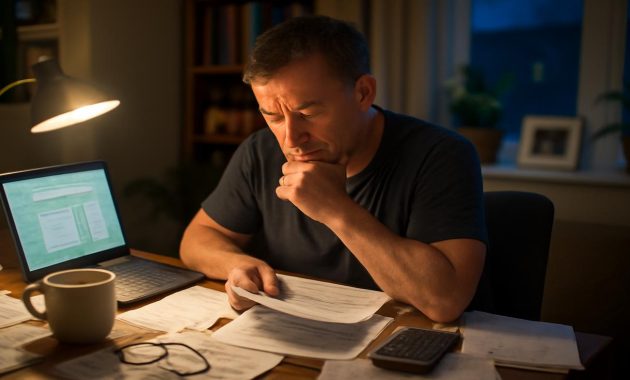

The first time Lena noticed the knot in her stomach, she was standing in the humming fluorescence of a supermarket aisle, staring at a row of olive oils that all looked the same but cost wildly different amounts. Her cart held the same groceries she bought most weeks: pasta, tomato sauce, frozen vegetables, a small pack of chicken thighs, a guilty bag of coffee-shop-quality beans she refused to sacrifice. Her paycheck had cleared that morning. The rent was already scheduled, the utilities set to auto-draft. On paper, she was fine. She was even putting a sliver of money into a retirement account. Yet as she compared prices and did quiet math in her head, the feeling washed over her again: I’m behind. Behind who, she couldn’t quite say. But definitely behind.

The Quiet Creep of “Not Enough”

If you listen closely, you can hear it in everyday places—the soft rustle of financial anxiety. It lives in the pause before a friend glances at the bill on a restaurant table. It’s in the way your hand hovers over the “Place Order” button on an online cart. It’s in the hollow feeling on payday when your checking account blooms for a moment and then shrinks as bills pull their automatic share.

For many people, the story on paper looks pretty decent: a steady job, a bit of savings, a retirement plan that has more than zero in it, debt that, while annoying, is at least being chipped away. Progress is happening. But emotionally, it doesn’t feel like progress. It feels like running on wet sand—moving, technically, but never quite catching up to the solid ground everyone else seems to be walking on.

So what is this strange dissonance? Why do so many people feel financially behind, even as the numbers suggest small, steady steps forward? Part of the answer lives in the math. A big part lives in our brains. And another part lives out there in the culture swirling around us, whispering that other people are doing better—faster, cleaner, with much nicer lighting.

The Invisible Baseline We Keep Chasing

In the cool glow of an evening living room, you open your favorite social app. A high school classmate, once as broke and lost as you, just posted about closing on a house with a wide porch and a yard big enough for a dog to sprint in circles. Someone else is on their second trip to Europe this year. Another friend just shared a screenshot of their investment portfolio “milestone.” You know it’s curated. You know people don’t post their overdraft fees or the nights they ate cereal for dinner. And yet, the seed gets planted: I should be farther along.

Most of us carry an invisible baseline of what “doing well” should look like. Maybe it came from our parents, who bought their first home in their twenties, when housing was less expensive compared to income. Maybe it’s shaped by movies where 27-year-olds live in spacious apartments with city-views and suspiciously low rent. Maybe it’s the subtle expectations of your industry, your city, your friend group.

This baseline is rarely examined directly. It hums along in the background like the fridge in your kitchen—always on, barely noticeable, until the room falls quiet and you suddenly hear it. You might not have written down that by age 30 you should own a home, have no student debt, take one big vacation a year, and keep six months of expenses in savings. But if that’s the mental picture you’ve absorbed, anything less than that feels like falling short.

Here’s the twist: as you make financial progress, the baseline often moves. A promotion arrives; suddenly “doing fine” looks more expensive. You move to a nicer neighborhood; now everyone’s “normal” includes things you didn’t grow up with. Lifestyle expectations drift upward as quietly as steam rising from a mug of coffee. You don’t always see it happen. You just feel like you’re never quite catching up.

When Numbers Say “You’re Okay” but Your Body Says “Panic”

There’s a peculiar moment many people experience: you open your banking app, take a breath, and the numbers greet you with something that, objectively, isn’t a crisis. There’s money there. The credit card is not maxed out. The bills are scheduled and should clear. And yet, a tense heat spreads under your skin. Your shoulders creep toward your ears. The voice inside says, We’re still not safe.

This mismatch between reality and feeling is not a personal failure. It is, in many ways, biology. Our nervous systems evolved in a world where scarcity could mean literal danger. Famine. Harsh winters. No backup plan except the tribe around you. In that world, the brain that stayed hyper-alert to threats—real or potential—had a survival edge.

Fast forward to modern life, where “threat” often looks like a rent hike, a medical bill, or an unexpected car repair. The fear can be just as intense, even if it’s not life-or-death in the old-fashioned sense. Your body doesn’t know the difference between “I might not be able to cover this surprise bill without dipping into savings” and “I might not eat this week.” It just senses uncertainty and flares into alarm.

Over time, if you’ve lived close to the edge—even once—it can leave an imprint. Maybe you’ve bounced a payment in the past, or carried a balance that seemed immovable, or watched your parents argue over money. Those memories become quiet landmines. Even when things are improving, your nervous system might not get the memo. It’s still scanning for disaster, seeing shadows where there are only awkward inconveniences.

The result? You feel behind, not because your numbers are catastrophic, but because your body has learned to associate money with threat. Until that gets acknowledged—gently, without shame—no spreadsheet will fully soothe you.

The Strange Logic of Progress That Doesn’t Feel Like Progress

In theory, progress should feel like relief. You earn a bit more, pay down some debt, nudge up your savings. The cliff edge gets farther away; the ground a little more solid. Then why does it sometimes feel like running in place?

Part of the answer lies in how financial progress actually works: slowly, unevenly, with a frustrating amount of backtracking. Real life is lumpy. Raises don’t always line up with rent increases. You pay off one loan and a medical bill arrives. You finally build an emergency fund, and your car decides it’s time to introduce itself to the mechanic again.

Progress, in other words, does not feel like a straight staircase. It feels like a forest trail—up, down, looping back, occasionally vanishing under leaves so thoroughly you wonder if you’re even on it anymore. From a distance, if you map it, you can see you’re moving forward. But walking it, breath in your lungs and sweat on your back, it’s hard to feel triumphant when you’ve just hit another incline.

There’s also the invisibility factor. Many of the smartest financial moves don’t look like much from the outside. Paying off a credit card feels like erasing a mistake, not gaining something new. Putting money into a retirement account is sending it off to a future self you can barely imagine, instead of getting something tangible today. Staying in a smaller apartment longer, keeping the older car, saying no to one more weekend trip—these choices are powerful. But they don’t give you that flashy, satisfying “I made it” signal. They’re quiet wins, and quiet wins are easy to overlook.

The World Around You Is Louder Than Your Inner Progress

Step outside, physically or digitally, and you walk into a theater of comparison. The cues are everywhere: billboard families laughing on perfect sofas, colleagues casually mentioning their home renovations, influencers turning “a chill week” into a sequence of restaurants, outfits, and micro-luxuries. It’s not only marketing—it’s the social air we breathe.

Money, in this context, stops being just a tool and starts becoming a mirror. What you can afford becomes tangled up with what you’re worth. A tiny apartment, a dented car, a secondhand couch—they can start to feel like verdicts instead of circumstances. Even when you intellectually know better, the emotional residue lingers.

Then there are the big, heavy forces you can’t see directly: wage stagnation in certain fields, housing costs that outpace incomes, student loans that swallow starting salaries, healthcare costs that hover like storm clouds. You might be working as hard—or harder—than previous generations, but the math you’re playing with is harsher. Progress is real; it’s also running against a current that your grandparents didn’t always have to swim in.

So you end up with a two-layered reality. On one layer, your personal progress is genuine: you’ve negotiated a raise, automated savings, tackled debt, made smarter choices than you did five years ago. On another layer, your progress is being measured against an environment tilted toward feeling behind. The benchmark isn’t just financial security; it’s a moving, shimmering ideal of “success” that’s been professionally designed to stay just out of reach.

Rewriting the Story of What “Ahead” Actually Means

Imagine, for a moment, stepping outside of all of it. The comparisons, the old baselines, the ads that pretend everyone your age owns a plant-filled loft with perfect lighting. Imagine that none of those things get a vote. What would “ahead” look like then?

Maybe it looks smaller than the picture in your mind. Not a house, yet—but the sense that your rent is manageable. Not a fully funded retirement—but the habit of putting in something, month after month. Not zero debt—but one less bill weighed down by interest. Fewer emergencies that blow up your life; more inconveniences that you can meet with an exhale and a plan.

This shift sounds subtle, even disappointingly modest. But it can be radical: redefining “ahead” as “more stable and more aligned with my values than last year,” rather than “matching some composite image of what a financially successful person should have by this age.” It doesn’t mean shrinking your dreams. It means making your progress visible to yourself, instead of invisible behind someone else’s scoreboard.

One practical way to see this is to map your own trail instead of everyone else’s highway. When you track your life against your own past—What did my savings look like two years ago? How stressed was I about money five years ago?—you often discover that you’re not stuck. You’ve been climbing all along.

Numbers, Feelings, and the Quiet Power of Reframing

For people like Lena, standing in that grocery aisle, the bruise isn’t only in the budget. It’s also in the story she’s telling herself: that everyone else has it figured out, that she somehow missed a class where adults learned how to be “on track,” that her progress is too small to matter. But if you change the angle, the same life can tell a different story.

The table below offers a simple way to notice this reframing in action, by contrasting how financial progress often feels versus what might actually be true underneath.

| What it feels like | What might also be true |

|---|---|

| “I’m still living paycheck to paycheck.” | Your expenses are covered, and you’re building skills or experience that could boost income over time. |

| “My savings barely exist.” | You have more saved than you did a year ago, even if it’s small. The habit is forming. |

| “My debt is still huge.” | Your total balance is down from its peak; interest is shrinking; momentum is quietly on your side. |

| “Other people my age are so far ahead.” | You’re comparing your unedited life to their highlights; their private struggles are invisible to you. |

| “I keep making money mistakes.” | You’re learning from past choices and already making different ones. That is long-term progress. |

This isn’t about positive thinking wallpapering over legitimate stress. It’s about letting the full truth in: that progress and fear can coexist; that “not where I want to be yet” can live alongside “much farther than I used to be.” Your nervous system, tuned for threat, may only highlight the gaps. You may have to deliberately point out the gains.

Living Forward Without Feeling Forever Behind

Picture an evening a few years from now. Maybe you still don’t have everything the culture told you to want by this age. Maybe the house arrived later than expected, or not at all. Maybe the student loans took longer to tame. Maybe your savings grew in slow, almost boring increments.

But imagine this: your rent or mortgage is a number that doesn’t make your chest tighten. You have some buffer in the bank, imperfect but real. When the car makes an ominous clunk, you sigh rather than spiral. You open your banking app and, for once, your body doesn’t instantly brace for bad news. It just…looks. And in that quiet moment, you realize you’re not living at the edge of a cliff anymore. You’re on a trail. It still goes uphill. But it’s walkable.

This is what many people are actually building, step by unremarkable step, even as they feel behind. They’re not failing. They’re living through a time when the cost of “normal” life is high, the pressure to look successful is unrelenting, and the brain is wired to panic first and notice progress later.

Feeling behind financially, despite real progress, doesn’t mean you’re bad with money or destined to struggle forever. It means you’re human in a culture that makes calm about money surprisingly hard to come by. The work, in part, is outer—earning, saving, paying down, choosing. But it is also inner: loosening the grip of those invisible baselines, teaching your nervous system that “enough for today” is not the same as “in danger,” letting small steps count as steps, not as failures to be farther ahead.

The next time you’re standing in a grocery aisle, or scrolling past someone else’s milestone, or running your thumb over the edge of a bill you wish were smaller, you can try a quiet experiment. Ask, not “Why am I so behind?” but “Where, exactly, am I now compared to five years ago?” Trace the trail: the debts that no longer exist, the crises you survived, the raises you negotiated, the habits you fought hard to build.

The story might not change overnight. The knot in your stomach might loosen only a little. But each time you notice the real, messy, non-glamorous progress you’ve made, you tug a thread in the old narrative. Over time, it can unravel. In its place, a new story can emerge—one where you’re not racing an invisible clock or chasing someone else’s version of “ahead,” but moving, steadily, in the direction of a life that actually fits you.

Frequently Asked Questions

Why do I feel broke even when I’m paying my bills?

You can feel broke because your nervous system is wired to notice risk more than safety. If you’ve lived close to the edge before—or you’re surrounded by people who seem to have more—it’s easy for “I’m covering my basics” to still feel like “I’m not safe.” The feelings often lag behind the facts.

How do I know if I’m actually behind financially?

Instead of comparing yourself to others, look at a few concrete markers: Are you paying your essential bills on time most months? Is your total debt trending down or at least not growing? Are you saving anything at all, even a small amount? If the answer is yes to some of these, you’re likely making real progress, even if it doesn’t feel dramatic.

What can I do to feel less anxious about money?

Simple routines help: track your cash flow for a month, automate one small amount of savings, and schedule a regular “money check-in” time so you’re not constantly worrying in the background. On the emotional side, notice when you’re comparing yourself to others and gently bring the focus back to your own past progress.

Is it normal to feel behind compared to friends?

Very. People share highlights, not full stories. You see their vacations and house purchases, not their quiet anxiety, family help, or debts. Different families, careers, and cities create different financial timelines. Feeling behind doesn’t mean you actually are—it often means you’re comparing across completely different starting points.

How can I measure my progress in a more realistic way?

Compare yourself to your own past, not to other people. Look at where your savings, debt, and income were two or three years ago. Track small improvements—like paying one bill on time every month, reducing a credit card balance, or building a small emergency fund. These are real markers that your life is becoming more stable, even if they don’t look dramatic from the outside.